The Option Greeks

Yes, those weird symbols you find in equations

There’s no questioning the popularity of Greek letters to represent variables or special functions in math and science. Part of it has to do with their international recognition and compactness (that is, they can easily represent complicated ideas. Think of what π describes: the ratio of the circle’s circumference to its diameter), but another reason is simply historical tradition. Pioneering ancient Greek thinkers such as Pythagoras and Archimedes used these letters in their work, and people since then decided to keep it.

As it grew more integrated with mathematics over the years, finance adopted Greek letters to denote various measurements, particularly in options pricing. These symbols help investors and analysts factor in different components such as the underlying asset’s price, time until expiration, and implied volatility when valuing options. In this article, we’re going to look at 3 key Greek letters used in finance.

Delta Δ

This is basically how sensitive the option’s price is relative to changes in the underlying asset’s prices. Specifically, the rate of change between the option’s price and a $1 change in the underlying asset’s price. Expressed as a percentage between 1 and 0 for a call option (with 1 representing a 1:1 correlation in price movements) and -1 and 0 for a put option (with -1 representing a 1:1 correlation in price movements), the delta measures the option contract’s exposure to the underlying asset’s price.

The delta is also used to value the option as a security because it can help guess whether an option will expire in the money (possess intrinsic value). As an option moves further into the money, the delta value moves further from 0 (heads toward 1 for call options and -1 for put options). Here’s an example to illustrate why: say you have a stock call option with a strike price of $100, but the actual stock price is $25. In other words, this option is way out of the money (possesses no intrinsic value). Now say the underlying stock price doubled from $25 to $50 – should we expect the call option price to also double? Not at all, because it’s still way out of the money even if the underlying stock is $50. Hence, that option’s delta is low because it’s unlikely for the stock price to increase its value x4 and possess any value.

(Side note: just to clarify the terminology, a long option means you’re buying an option from someone whereas a short option means you’re selling an option to someone).

Deltas are positive for long call options (where the contract holder has the right to buy the underlying asset at a predetermined price) and short put options (where the contract issuer is obliged to buy the asset at a predetermined price if the option buyer chooses to sell the asset). The value of a long call option increases when the underlying asset’s price increases because the option holder can then buy the underlying asset at the predetermined price, which is presumably lower than the asset’s price. Short put options are also more valuable when the underlying asset’s price increases because then the option holder wouldn’t want to sell their assets to the option issuer at the strike price, as it’s presumably lower than the market price. And so, the option holder wouldn’t sell anything and the option issuer would keep the premium without having to buy anything.

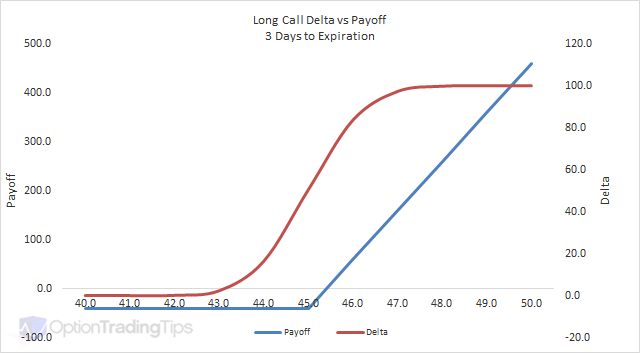

This option’s strikethrough price is $45, which is why the payoff line starts increasing after that point on the x-axis. Notice how the delta only increases around the at the money price range (where the option’s strike price is around the underlying asset’s market price), but then flattens when the option is either in the money or out the money. Also, the payoff line is completely flat before the $45 mark – that’s because the most you can theoretically lose with a long call option is the premium you paid for it.

The maximum loss for a short put option is unlimited since if the underlying asset’s price keeps falling then the option purchaser can simply sell the asset to you at the strikethrough price, whereas the maximum profit is the premium you earned when selling the option. In this case, the strike price is $60.

Conversely, deltas are negative for short call options (where the contract issuer is obliged to sell the asset at a predetermined price if the option buyer chooses to buy the asset) and long put options (where the contract holder has the right to sell the underlying asset at a predetermined price). The value of these options decrease when the underlying asset’s price increases because if the strike price is below the market price, the investor may have to sell the asset at a discount.

Similar to short put options, short call options have an unlimited theoretical loss since the price of the underlying asset can simply continue to rise above the strike price, whereas the maximum profit is the premium paid by the option buyer.

Again, just like the long call option, the most you can lose in a long put option is the premium you paid to buy it. But once the underlying asset begins to drop below the strike price of $45, the option turns into the money as the investor can then sell the asset for more than the market price.

Gamma Γ

Sometimes confused with delta, an option’s gamma is the rate of change between an option's delta and a $1 move in the underlying asset's price. Think of it as a second-order metric of price sensitivity. Because gamma measures the delta’s movement with respect to the underlying asset’s price, it’s often used to determine how stable an option's delta is, with high gammas implying that the option’s delta could dramatically change with a small movement in the underlying asset’s price.

Like the delta, the gamma’s value depends on the kind of option. Long call options and long put options have positive gamma because their deltas correlate with that of the underlying asset’s: an increase in price will increase the delta. Keep in mind that this doesn’t change either the long call option or the long put option’s delta value – when the underlying asset’s price increases, the long call option’s delta moves towards 1 whereas the long put’s delta moves towards -1. On the other hand, gammas are negative for short call options and short put options, because their deltas are inversely correlated with the underlying asset’s price movements.

Time is also very important in determining an option’s gamma; the further the option is from expiring, the smaller the gamma. This makes sense when considering time’s effect on delta; options with longer expirations have more time to expire, and so their prices are influenced by factors other than the underlying asset price (unexpected crashes or rallies, shifting financial conditions, etc). The delta has a smaller rate of change with longer expirations, and a larger rate of change with shorter expirations (which is why higher gammas indicate more volatile deltas: higher gamma = shorter expiration = more volatile delta).

Lastly, the option’s moneyness (how much in or out of the money the option is). As stated previously, when an option becomes more in the money, its delta moves towards either 1 (for long call options and short put options) or -1 (for short call options and long put options). Either way, it means that the gamma will decrease because the option’s delta can’t move past 1 and -1. The same can be said for out of the money options: the deltas will approach 0, and since it can’t get past 0, the delta volatility will decrease, thereby decreasing the gamma.

Thus, an option’s gamma will peak when it’s around at the money (so around 0.5 or -0.5) because that’s when the option’s delta can change the most.

As shown in the graph above, gamma is affected by both time and moneyness. The green option’s gamma doesn’t change much around the strike price, whereas the black option does. The reason is the time difference – the green option has 9 months of other variables other than the delta that could affect its price, whereas the black option only has 3 months.

Theta θ

The eighth letter of the Greek alphabet, theta is the option’s time decay – how much the option’s price will decrease as it approaches the expiration date. There’s a simple but important rule of thumb to keep in mind regarding options and time: longer-dated options are worth more than shorter-dated ones because the more time left until expiration, the more opportunity there is for the underlying asset’s price to suddenly increase or decrease, and then for the option to become in the money. Time decreases an option’s value – it quite literally reduces the opportunity for favourable price movements in the underlying asset.

This is why theta is a negative value for long options and a positive value for short options. Long option holders have time working against them, with each passing day depleting their option’s value, resulting in a negative theta value. But short option holders want the option they sold to decrease in value because an option that’s decreasing in value means the option holder is unlikely to exercise it, allowing the option issuer to simply profit with the premium.

With that in mind, options have 2 kinds of values: an intrinsic value and a time value. The intrinsic value is the amount of money you’d gain if you immediately exercised the option, whereas the time value describes the value of being able to exercise the option some time in the future (i.e. the expiration date is further away). This means that even an out of the money option will have some time value, since there’s a chance the underlying asset’s price could move above or below the strike price.

However theta is also affected by the option’s moneyness, just like delta and gamma. At the money options have a 50/50 chance that it’ll end up in the money by expiration, and this uncertainty increases the theta value. But as an option moves deeper either in the money or out of the money, the chances of its value significantly changing by expiration decreases, therefore decreasing the theta.

Econ IRL

Filing taxes electronically seems a no-brainer. It’s easier, saves a ton of time, and far more convenient than having to mail everything to the government. But while the average citizen will certainly appreciate these perks, are there perhaps any more significant societal gains from having the mass population file their taxes electronically? This week’s paper asks just that.

Using a randomized control trial with a group of randomly selected firms from Tajikistan, the author found that compliance costs were reduced by 40%. Nothing surprising there, as people could do their taxes from their desks as opposed to having to walk to the tax office. As for the more pressing issue of tax fraud and corruption, firms that were more likely to evade tax under a paper-filing system paid double the amount in taxes under an electronic system.

Weirdly enough, firms less likely to evade taxes paid less when e-filing their taxes. But given how these particular firms also paid fewer bribes, it’s also likely that e-filing reduces extortion opportunities for both firms and the tax collectors.

‘Till next time,

SoBasically