The 2022 Nobel Prize in Economics

The former Fed Chair and...2 others

At a time when the CEO of JPMorgan Chase, Jamie Dimon, warns of a world recession in 2023, announcing the year’s Nobel Laureates in Economics for their work on financial crises seems to be a suitable decision. Nevertheless, a big round of applause goes to American economists Ben S. Bernanke, Douglas W. Diamond, and Philip H. Dybvig for receiving the 2022 Nobel Memorial Prize in Economic Sciences. In commemoration of their awards, we’re going to go over each of the recipients’ accomplishments and lasting contributions in economics.

Fed Chairman Bernanke

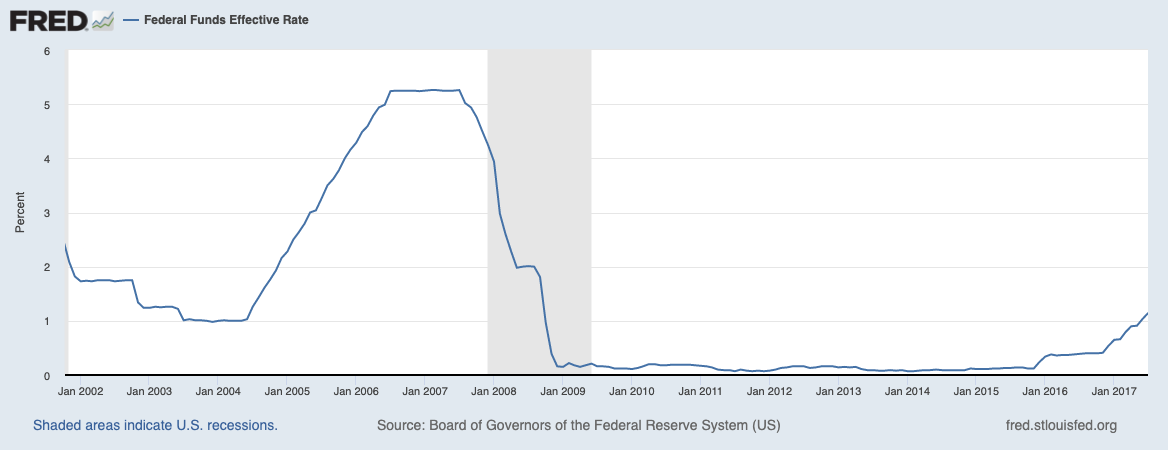

This is by far Bernanke’s claim to fame; not only serving as the 14th Chairman of the Federal Reserve, but doing so right in the middle of the 2008 financial crisis. Given the magnitude of the situation, Bernanke was forced to adopt some drastic moves and unorthodox measures. On September 18, 2008, Bernanke and Treasury Henry Paulson met with Speaker of the House of Representatives Nancy Pelosi and demanded a $700 billion emergency fund. This giant sum of money later became known as the Troubled Assets Relief Program (TARP) and its purpose was to relieve the markets of toxic assets and increase overall liquidity.

Almost 2 months later, he lowered interest rates to 0%. Considering how rates were above 5% just a year ago then, this is no small deal.

After deciding that neither the interest rate cuts nor the TARP bailout was enough, Bernanke implemented 3 rounds of quantitative easing wherein the Federal Reserve purchased $4.5 trillion in bank debt, mortgage-backed securities, and Treasury notes. More than a decade later, Bernanke’s actions continue to be hotly debated with supporters saying he helped prevent the Great Recession from becoming a Great Depression and critics arguing that suppressing interest rates to historic lows and flooding the economy with easy credit are partly to blame for today’s soaring inflation.

Pre-Fed Chairman Bernanke

People are not usually awarded Nobel Prizes solely for holding a government position, no matter how difficult or high-pressure their jobs were. Bernanke is no exception. His classic paper, published in 1983 is titled "Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression." In this thesis, Bernanke builds on economists Milton Friedman’s and Anna Schwartz’s study of the Great Depression by focusing on banks instead of the money supply.

Banks are a financial intermediary, that is to say, they connect those who supply funds with those who demand thereof. So when their costs of doing business rise, they must also raise the cost of borrowing (i.e. the interest rate for loans). In the case of the Great Depression, financial disruptions increased the costs of banks’ business operations, and thus the cost of credit, which then further decreased aggregate demand. When the economy is facing mild downturns, banks have every incentive to avoid risky ventures – such as giving out loans – and when they do, they charge more interest to compensate for the greater risk.

With less loans being given out and thus less people having access to capital, the economy is further weakened. Eventually, the cost of acquiring credit simply becomes too expensive, which then dwindles aggregate demand. This cycle of economic decline and scarcer access to capital, what Bernanke referred to as the financial accelerator, is a key reason for the Great Depression’s unusual length and severity.

Along with providing a new perspective on the worst economic crisis in history, Bernanke’s thesis highlighted an important link between the real economy and financial markets. All it takes is a small change in financial markets to produce a large change in economic conditions. His research in this area is partly why people thought of him as the perfect candidate for Fed Chairman back in 2006 - the Great Depression and the macro-financial mechanisms behind it was the main focus of his career.

The Diamond-Dybvig Model

Douglas W. Diamond, from the University of Chicago’s Booth School of Business, and Philip Dybvig, from first Yale and now Washington University in St. Louis, spent much of their academic careers as a dynamic duo. Their principal contribution was a model of bank runs and their related financial crises.

Published in a 1983 paper entitled “Bank Runs, Deposit Insurance, and Liquidity,” the model first pointed out how banks have a mix of illiquid assets (stuff that cannot easily and readily be sold without a substantial loss in value) such as mortgage loans (until CDO’s came into the picture, you couldn’t really “sell” mortgages to investors”) and liquid liabilities, in particular bank deposits, which can be withdrawn at any time and thereby suddenly result in the bank losing money.

Again, we need to understand banks as financial intermediaries between savers and borrowers, 2 groups with conflicting interests; savers want more money readily available (through their bank accounts) and borrowers want money being lent to them. As such, there are really 2 kinds of situations that can be derived from this. The first is under “ordinary circumstances”, with savers' needs for cash being random but more importantly, asynchronous. Because the number of withdrawals in the short term won’t grow to large amounts, a bank can afford to make loans over a long period of time and keep small amounts of cash at hand in case any depositors wish to withdraw.

But what about unordinary circumstances? Remember, banks can’t turn loans into cash easily because they’re long-term investments, so if all depositors wish to withdraw their funds at the same time, it goes without saying that the bank is indeed screwed. It’s extremely unlikely that the bank will have enough cash on hand to pay off their depositors for very long before going bankrupt.

This is called a bank run – when so many depositors withdraw their savings that the bank runs out of money. They often irreversibly destroy the bank’s reputation as a safe place to store money and it’s something that even the healthiest of banks are vulnerable to. Each depositor’s incentive to withdraw funds depends on what they expect other depositors to do, so all it takes is just the right number of people to begin demanding their money back. And that’s where the Diamond-Dybvig model’s second key contribution lies: it allows us to apply game theory analysis to bank runs.

If depositors expect others to withdraw their money only when needed, then it’s rational for them to follow suit. But if depositors are rushing to close their accounts, then it’s rational for other depositors to follow suit. Both of these scenarios are perfect examples of Nash equilibrium (when no one can increase one's own expected payoff by changing one's strategy while the other players keep theirs unchanged).

Policy Implications

When banks face a bank run in the real world, the conventional move was to shut down and initiate a suspension of convertibility, where they refuse any further withdrawals. While this does bar some depositors from their cash, it also prevents immediate bankruptcy (pun intended), since some of the bank’s loans will hopefully be paid off and thus allow them to continue paying off depositors.

Diamond and Dybvig had a better idea: set up a government-backed deposit insurance to pay depositors all or part of their losses in the event of a bank run. This not only provides depositors with financial safety, but also reduces the chances of a bank run occurring in the first place. Why do people participate in bank runs? Because they don’t want to lose their savings. But if there’s a government insurance program promising to pay back their losses, then the problem of bank runs is dramatically nullified from the depositors’ point of view.

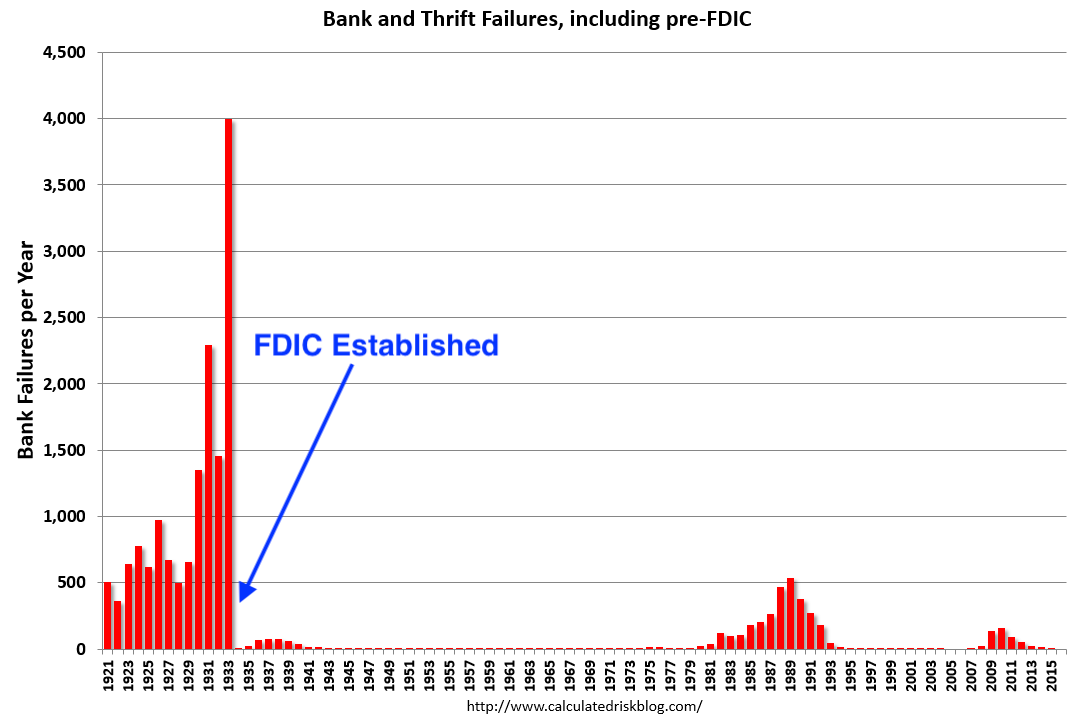

The Federal Deposit Insurance Corporation (FDIC) was established during the Great Depression and bank runs have become much more infrequent since then.

That and the surprisingly low cost – so long as bank runs are prevented, deposit insurance will never need to be paid out – are why the FDIC has garnered a lot of support. However, critics contend that the very idea of deposit insurance creates a moral hazard (when someone increases their risky behaviour because they don’t bear the full costs of that risk) since depositors have little incentive to take into account the financial health of their bank, resulting in more funds being available for weak and risky institutions at lower cost than would otherwise be the case. Additionally, banks may grow comfortable with using depositor money to undertake excessively risky investments since, if the borrower defaults, then the depositor insurance will simply make up for the lost depositor money.

Econ IRL

Urban transit infrastructure projects are huge investments typically costing hundreds of millions of dollars. The problem is measuring its benefits - it’s difficult to distinguish between the change in neighbourhoods as a cause of the new infrastructure with the change in neighbourhoods being the cause of something like neighbourhood composition. What’s needed is more individual-level data to assess the benefits or harms, caused by new infrastructure, on the neighbourhood’s residents.

This week’s paper focuses on a question leaning very much in that direction: are there indirect benefits from reduced labor market power from firms now that workers can substitute more easily between jobs? The short answer is yes; workers with access to transportation infrastructure are also given additional employment options, thereby reducing firm labor market power. Using a subway expansion in Santiago, Chile as a case study, the author finds that workers close to new subway stations start working further away, and even those who do not switch jobs start earning more, suggesting that employers have to try harder to keep their workers. Quantitatively, the labor market power reductions provide a 20-40% welfare gain for workers.

‘Till next time,

SoBasically