Marginalism and the Firm

An even more practical example

Those of you who read our last article on marginalism may have left wondering how such a seemingly abstract concept could possibly be relevant when analyzing the real world. But the truth is that marginal analysis is unknowingly employed by hundreds of thousands of businesses when analyzing and managing their production processes.

Picture an average coffee shop that, for the sake of simplicity, only sells cups of coffee. This shop has inputs (the resources used to produce coffee) and outputs (the actual cups of coffee). Focusing on the former, we can divide resources into 2 categories: fixed resources, meaning they don’t change even as you produce more coffee. Think about the coffee machines, the building, etc. You pay for these items once and then there’s no need to concern yourself with their cost for a while, regardless if you produce 1 cup of coffee or 1000 cups of coffee.

In contrast, variable resources depend entirely on your output. The more coffee you make, the more coffee beans, sugar, and milk you need. But the line between these 2 categories can get fuzzy real quick: at some point, depending on how much you use it, the coffee machine will have to be replaced. All machines go through wear and tear right? Does this therefore mean that the coffee machine is a variable cost? Even the building itself is likely to experience renovations sometime in the future.

This leads to another distinction: short-run production vs long-run production. A company is considered to be in the short run when they have at least one fixed resource (in this case, the coffee machine and the building). On the other hand, the long-run is more about what could potentially happen in the future, meaning that all resources (yes, even the coffee machine and the building) are considered variable in the long run.

Marginal Output

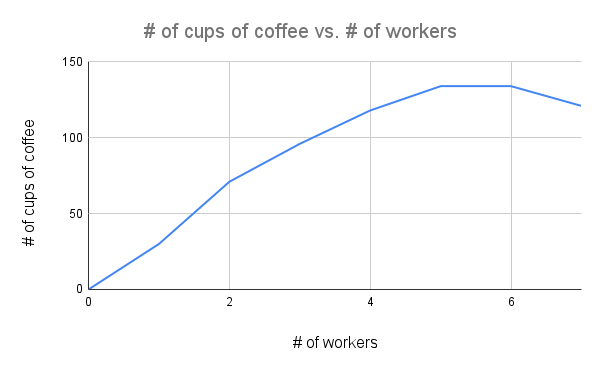

If we look at short-term production, an interesting pattern is quickly realized. If you have no workers in the coffee shop, then there’s no production. If you have just 1 worker, they have to do everything and so there’s no opportunity for the division of labor. But if we add 5 workers, then the coffee shop becomes more productive, with everyone specializing in what they do best and as a result, producing more.

The logic seems clear: more workers = more output. But there’s a limit to this. If we add 50 workers in the coffee shop, the place is going to be so crammed that no one will get their job done, resulting in decreasedproductivity and consequently, less cups of coffee being made.

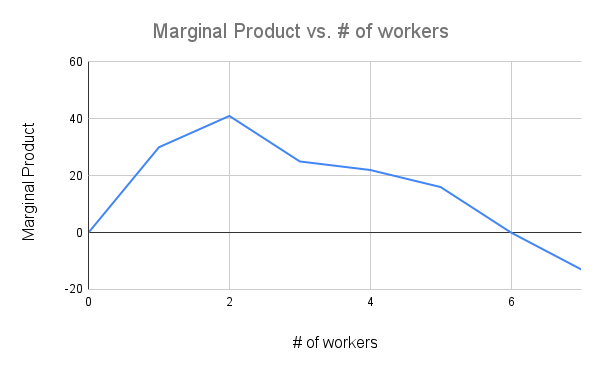

This is the law of diminishing marginal returns: as you add variable resources to fixed resources, the additional output will eventually decrease. Let’s see how it would apply to our hypothetical coffee shop:

Here’s what this chart is telling us: the first worker produces just 30 cups of coffee - that’s their additional output. But when 2 workers are in the shop, they both produce 71 cups of coffee in total, meaning that sending in another worker produces an additional 41 cups of coffee (71 - 30).

This jump in productivity highlights the benefits of specialization; with each worker focusing on what they do best, they’re both able to more than double the production. Adding a 3rd worker produces 96 cups of coffee, but the additional output drops to 25 cups of coffee. The 4th and 5th worker add in an additional 22 and 16 cups of coffee respectively. The 6th worker, however, has no effect on the total number of cups of coffee made nor the additional cups of coffee made.

No offence to worker #6 but they are effectively useless. Worker #7, on the other hand, is much worse. Throwing them into the mix actually decreases the total output to 121 cups of coffee, meaning their working takes away an additional 13 cups of coffee.

The important thing to keep in mind here is the difference between total and marginal returns. The total number of cups of coffee being produced was increasing up until worker #5, whereas the marginal return of cups of coffees (that is, how many additional cups of coffee are produced) has been decreasing since the beginning.

Marginal Cost:

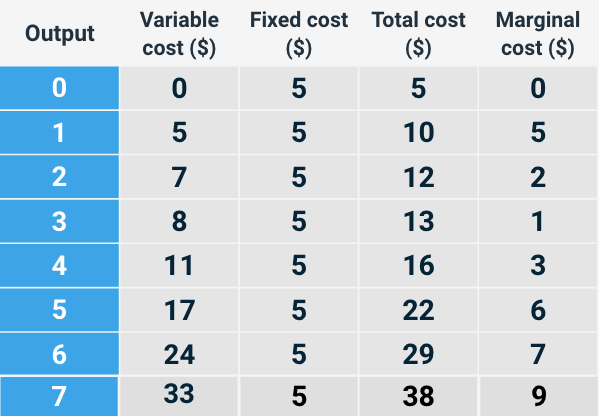

Remember our fixed vs variable resources distinction? Well for all businesses, resources have a cost - someone needs to pay for, in this case, the building, the coffee beans, sugar, milk, etc. Since resources have costs, economists often use the term fixed costs and variable costs when analyzing firms (fixed costs being ones that don’t change with the amount produced and variable costs being ones that change with the amount produced). Total cost, as the name suggests, is fixed costs + variable costs.

Like output, we can also apply marginalism to cost. Marginal cost describes the additional cost of producing one additional unit. Since we’re running a coffee shop, it’s the cost of producing one additional cup of coffee. It’s calculated by dividing the change in total cost by the change in output.

Looking at our coffee shop....

When we produce the first unit of coffee, the marginal cost of producing that additional unit is, just like the equation from earlier says, the change in total cost ($5) divided by the change in output (1), giving us a marginal cost of $5. Now that we have the marginal cost, we can calculate the per-unit cost, of which there are 3 types:

Applying these equations to our chart above, if we were to calculate the AVC, AFC, and ATC of 4 units, we would get $2.75, $1.25, and $4, respectively. We can verify this by adding up the AVC and AFC and seeing if it gives us the ATC (which it does; 2.75 + 1.25 = 4). After finding the AVC, AFC, and ATC of the other quantities too, let’s plot them on a graph with the marginal cost:

Observe the graph above and you’ll notice some broad trends:

The AFC becomes smaller and smaller because you’re taking the fixed cost (which is a set amount of money, in this case $5) and dividing it into smaller groups as quantity increases

The AVC goes down and up, hitting the MC curve at what’s known as the AVC minimum point

The ATC goes down and up, hitting the MC curve at what’s known as the ATC minimum point

MC goes down and up - remember the law of diminishing marginal returns

People often look at the more fundamental economic concepts especially as almost impractical and useless. Sure, the law of diminishing marginal returns is technically correct and all... so what? It’s true that most businesses don’t even sit down and draw some cost curve graphs to determine their optimal production rate.

What is true, however, are the broad ideas that we all implicitly know to be true. Why doesn’t Starbucks hire 100 workers for each restaurant to boost their coffee-making to the absolute max? Answer: law of diminishing marginal returns. Kevin Johnson, the CEO, probably isn’t going to respond with those exact words, but he (and others who haven’t read anything on economics) intuitively understand the basic idea of there being a limit as to how many resources you can input before output decreases.

The dismal science just helps us observe these already-understood theories in a systematic manner. In fact it is so systematic, that firms continually use them to maximize revenues as profits, as we shall see in our next article.